Do I Really Need Life Insurance?

Let’s face it. Most people put off buying life insurance for any number of reasons. Take a look at this list—do any of them sound like you?

- It’s too expensive. In the ever-burgeoning budget of having a family, things like day care and car payments and possibly even college tuition eat up a good chunk of the money each month, and a lot of people think that life insurance is just outside those “necessities” when money’s tight. But two things: life insurance is often not nearly as expensive as you might think, especially when you can get a good policy for less than the cost of a daily cup of coffee at the local café, and well, if money’s tight now, what if something happens to you?

People with no life insurance overestimate its cost by three times. And even those who have coverage, overestimate its cost by two times.1 While it is an expense that you have to budget for, imagine what the financial impact would be for your family if something were to happen to you and you had no life insurance coverage at all.

- That’s that stuff for babies and old people, right? People of a certain age remember Ed McMahon telling them their grandparents couldn’t be turned down for any reason and figure that’s the target demographic for life insurance. Or, you might have been offered a small permanent insurance policy for your newborn. The truth of the matter is that these are very specific insurance products—just as there are many insurance products for adults in their working and retirement years.

- I’m strong and healthy! You eat right, you stay active, and everyone admires how grounded and centered you are. You passed your last physical with flying colors! That’s GREAT! But you’re neither immortal nor indestructible. It’s not even that something could happen to you—though it could—so much as when you’re at your strongest and healthiest, there’s no better time to get a policy to protect your loved ones. If you fall seriously ill or suffer significant injury later, it will make it tougher to get that kind of policy, if any at all.

- I have life insurance through my job. Many people are offered life insurance as part of their employee benefit coverage –and often, it’s the first time they encounter life insurance and have no idea that a $50,000 policy, or one or two times their salary, isn’t as much as they think it is. It sounds like a lot of money (and it is!), until you realize that it has to cover some or all of the expenses for your loved ones in your absence. Plus, if you leave the job, it’s typically the type of insurance that doesn’t “move on” with you.

- I don’t have kids. Sure, kids are a big reason why some people get life insurance. But that’s not the only litmus test for needing protection. If there is anyone in your life who would suffer financially from your loss—your spouse or live-in partner, a sibling, even your parents—a life insurance policy goes a long way in making sure everyone’s still okay even if something happens to you.

- Life insurance—it’s on my list … eventually. There’s no deadline on life insurance, no mandate from the government on purchasing it. Your parents may have never talked to you about its importance, and it’s certainly not the most invigorating topic for conversation. But don’t let your “eventually” turn into your loved ones’ “if only.”

Information for this article was provided by Life Happens, a nonprofit organization dedicated to helping consumers make smart insurance decisions to safeguard their families’ financial futures: www.lifehappens.org.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments or products may be appropriate for you, consult with your financial professional.

Sources:

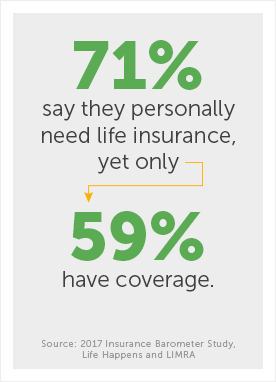

1The 2017 Insurance Barometer Study, Life Happens and LIMRA

Adult Financial Education Services (AFES)

September 2017

70 Comments

Aw, this was an exceptionally nice post.

Spending some time and actual effort to create a superb

article… but what can I say… I procrastinate a whole lot and never seem to get

nearly anything done.